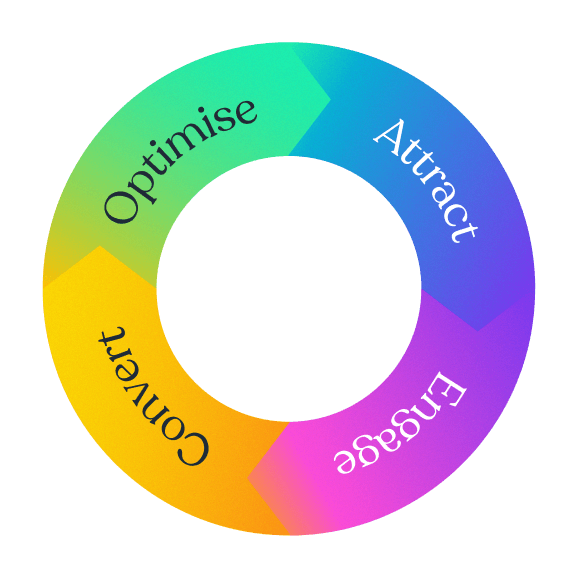

Attract.

D2I marketing amplifies the reach of your IR by up to 800%, bringing more eyeballs to your company and newsflow.

Engage.

D2I marketing increases the level of engagement of both prospective and current shareholders, thus increasing their conviction in your company.

Convert.

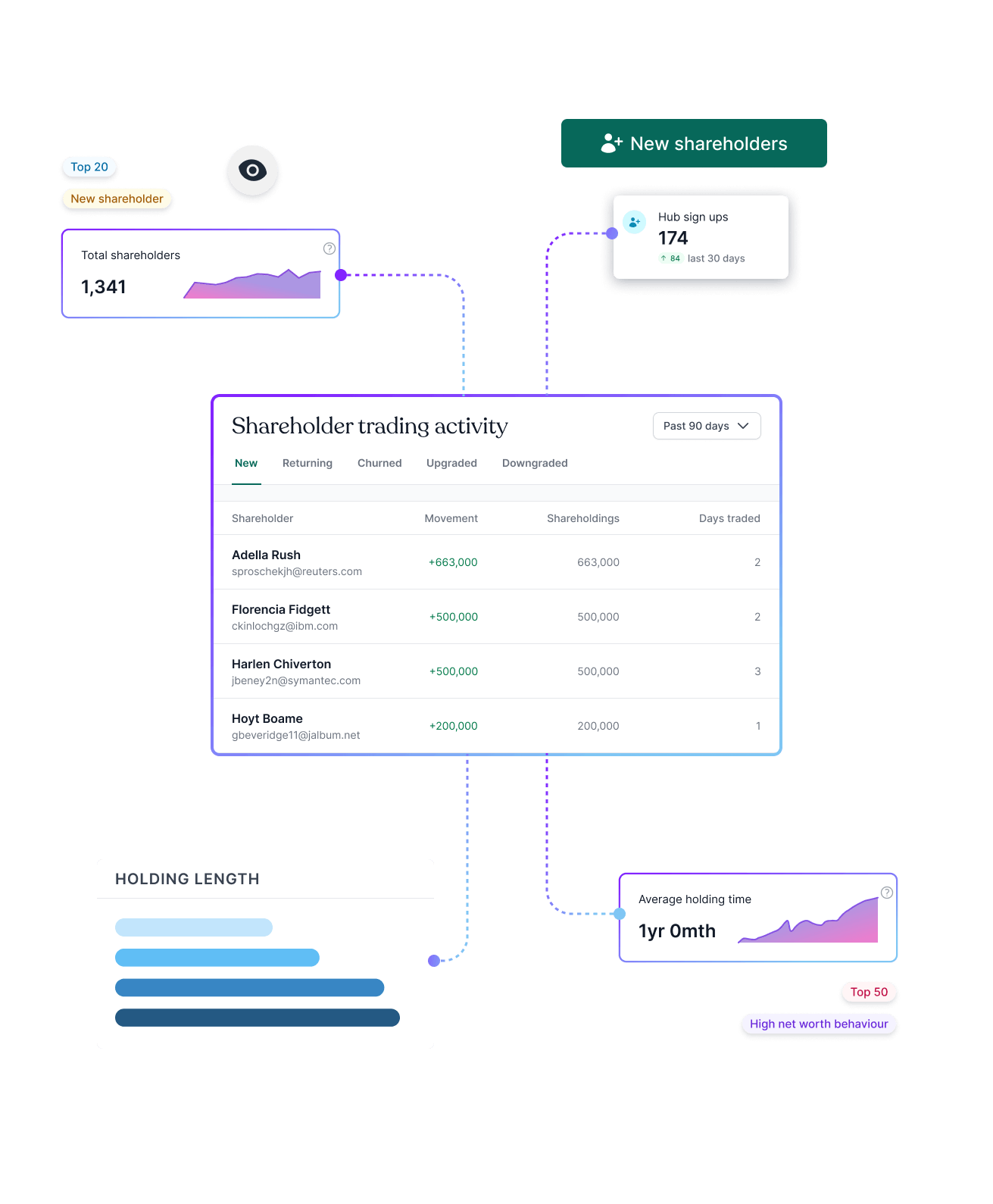

D2I marketing allows companies to adopt a data-driven approach to shareholder conversion. By owning the investor relationship, you can see the impact of newsflow and interactions on shareholder behaviour.

Optimise.

Leverage data and insights from communications, engagement, and trading behaviour to optimise newsflow and your IR spend and strategy.